10:00 pm Pacific

(Exclusive to BMR Subscribers – Not for Distribution or Posting on any Board!)

Gold eased off modestly during the 1st trading week of January, falling $17 an ounce to $2,045. This wasn’t surprising given how the greenback was due for a “dead cat bounce” out of temporarily oversold conditions.

A lower rate environment in 2024, combined with aggressive central bank buying and the strong prospect of a pick-up in investor demand thru ETF inflows, should bode extremely well for the yellow metal in the months ahead with John’s Gold chart in Canadian dollars suggesting we’ll see $3,300 (CDN) at some point this year ($2,736 was Friday’s close) which equates to about $2,500 U.S.

The $2,000 U.S. level could very well become the new floor for the yellow metal (certainly $1,900), so downside risk is limited to less than 10% while upside potential likely exceeds 20%.

The Establishment, and that includes the Federal Reserve, is going ALL-IN to get Joe Biden re-elected next November, so that means every effort to ensure a soft-landing in the U.S. economy. Restrictive monetary policy the last couple of years will become much more accommodating, just in time for the U.S. election season as the threat of another Trump Presidency ramps up.

Markets see a two-thirds chance (vs. a >80% chance a week earlier) of a first rate cut in March, according to CME’s FedWatch tool. However, what many investors overlooked is that Friday’s slightly “hotter-than-expected” jobs report for December (217,000 vs. the consensus estimate of 170,000) included 52,000 jobs created by the government sector and another 59,000 from the health care and social assistance sector which relies heavily on money from government spending. The economy under President Biden “added back” all the jobs it lost during the pandemic, no tremendous feat, and has “created” only 4.86 million new jobs since February 2020, a rather ho-hum result (just over 100,000 jobs a month). So the labor market is okay but not really as strong as the mainstream media suggest, setting up the Fed for a series of rate cuts in 2024 – especially if Oil prices (a key igniter of inflation in 2021 and 2022) remain in check.

There hasn’t been a better time to accumulate Gold and Gold stocks since late 2015 or the spring of 2020 during the height of the COVID crash. Selectivity is key, but fortunes are being born right now.

Short-Term Gold Chart

Gold has cleared, temporarily at least, key measured Fib. resistance at $2,029. This level now coincides with uptrend support on the short-term chart as RSI(14) also bounces along support.

Any minor pullback in Gold to start 2024 should be pounced on, as we stated last weekend. As January progresses, bullion has a great chance to reach into new record high territory above $2,100.

Gold In Canadian Dollars

The key takeaway here is that the $2,500 (CDN) level (~$1,885 U.S.) held throughout 2023 and this isn’t going to change in 2024.

Gold finished 2023 at $2,739 (CDN) and held steady in the 1st trading week of 2024, giving up just $3 an ounce to close Friday at $2,736.

Measured Fib. at $2,645 has consistently been a key resistance level for Gold in loonie terms. What has occurred appears to be a major breakout above $2,645 and the start of a move (2024) toward next measured Fib. at $3,314 (~$2,500 U.S.).

Any dip below $2,650 would likely be brief and shallow given the support of the SMA-200, currently $2,664 on this long-term weekly chart.

How soon Gold can get to $3,314 (CDN) is a matter of debate, but that’s certainly a logical minimum price target for 2024 (~$2,500 U.S.).

TSX Gold Index

The TSX Gold Index closed Friday at 276, off 8 points for its 2nd straight weekly loss.

Gold producers have strong balance sheets and many are pumping out impressive amounts of free cash flow at current Gold prices, such as Lundin Gold (LUG, TSX) which has reported over $200 million (U.S.) in free cash flow the last 2 quarters.

Weakness in Crude Oil is bullish for Gold producers as Oil is a big part of their cost structure.

The Gold Index dropped as much as 29.2% from its May 4 high of 345 to a crazy October 3 intra-day low of 244.

The bottom is in:

- RSI(14) breakout above its downtrend line from Q2

- RSI(14) is expected to gain traction above 50%

- Exceptionally strong support exists from the 1,000-day EMA, currently 278, to 260

- 280 (Fib.) is a key breakout point – the Index has temporarily fallen back below this level

- ADX indicator continues to show a neutral trend with -DI back above +DI

China Buying Continues To Support Gold

- Central banks added a net 42 tonnes to global official Gold reserves in October

- The People’s Bank of China was again the largest buyer, followed by the Central Bank of Turkey and National Bank of Poland

- October saw higher sales volumes compared to the previous 2 months – led by Uzbekistan and Kazakhstan.

Central banks’ Gold buying slowed in October but did nothing to alter the overall trend of robust buying that has captured the attention of Gold investors. Reported global net purchases totalled 42 tonnes during the month, 41% lower than September’s revised total of 72 tonnes, but still 23% above the January-September monthly average of 34 tonnes.

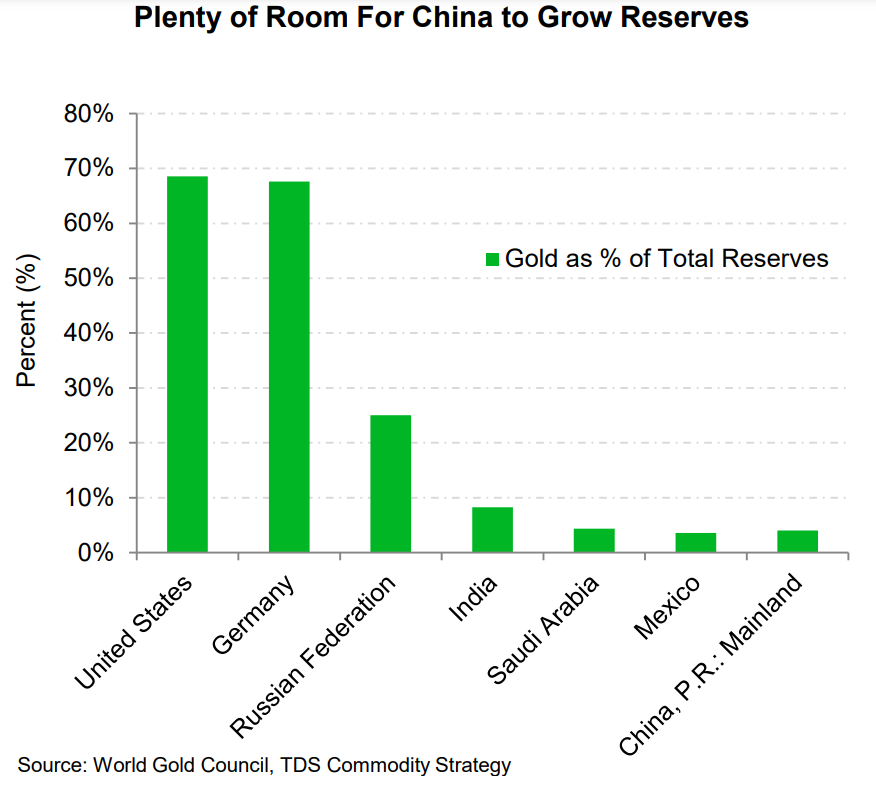

Country-level activity followed a familiar theme: A small number of banks accounting for the global total. The People’s Bank of China remained the largest purchaser, reporting the addition of 23 tonnes of Gold to its reserves – the 12th consecutive monthly addition. This brings its YTD net purchases to 204 tonnes and lifts its reported Gold reserves to 2,215 tonnes. Despite the significant increase, reported Gold reserves still account for just 4% of the bank’s total international reserves.

China’s ongoing Gold purchases have put renewed focus on the growing de-dollarization trend as nations around the world reduce their exposure to the U.S. dollar. Although China has become a leading buyer in the precious metal market, some analysts say that the central bank is just getting started.

“When you buy Gold, it’s a direct vote against the U.S. dollar,” stated Willem Middelkoop, creator of the Commodity Discovery Fund. “China is sending a message to the White House that they don’t support the global financial system backed by the U.S. dollar.”

Middelkoop said he also expects China to buy Gold for an extended period, and that he believes this is the start of the end game for the U.S. dollar.

Thorsten Polleit, chief economist at Degussa, said he also sees China’s sustained Gold purchases as a vote of no-confidence in the greenback.

“China is sending an unmistakable signal to the world for all eyes to see: It reduces its U.S. dollar holdings and, at the same time, increases its Gold reserve stock,” he said. “Like many other non-western countries, China wishes to reduce its dependence on the greenback, and physical Gold is the greenback’s natural substitute.”

Through the 1970’s, Gold as a percentage of global central reserve assets averaged about 40%. Today, the average is just above 15%. If Gold reserves were to get back to levels last seen more than 50 years ago, $3.2 trillion would flow into the precious metals market.

Even though China’s central bank has been buying steadily and in large quantities, the 4% that Gold represents of its $3.115 trillion in reserves remains very low.

Silver Short-Term Chart

John’s short-term Silver chart shows exceptional support just above $23 (uptrend line + Fib.) with key resistance at $24.59.

Multiple moves above $24.59 in 2023 were fairly brief with traders selling heavily into those situations.

Silver must conquer $24.59 and then hold that level for a sustained period in order to build upside momentum. We believe that will occur during the 1st quarter or 1st half of 2024.

Silver finished 2023 Friday at $23.17, off half a point from the previous week’s close.

Silver Long-Term Chart

Silver’s long-term chart holds very strong encouragement for Silver bulls.

The primary trend remains bullish despite the general weakness after the March/April/early May rally.

- Confirmed RSI(14) breakout above downtrend line going back to late 2020

- Price action since 2020 is defined by a bullish flag with the top of that flag cutting through the key $24 area – confirmed breakout pending

- +DI is modestly above -DI, but ADX trend indicator is officially “neutral”

- Sell pressure (CMF), dominant through most of 2021 and 2022, transitioned into low buy pressure in 2023

- Watch for “The Big Breakout” by early 2024

Bullish Silver Supply-Demand Dynamic

Investors could finally be waking up to a massive imbalance in Silver supply and demand fundamentals as demand continues to outstrip supply, according to the latest report from The Silver Institute.

In mid-April the Institute published its 2023 Annual World Silver Survey, and according to the research, Silver saw its most significant market deficit on record, hitting 237.7 million ounces. Metals Focus, the firm behind the research, noted that the deficits in 2021 and 2022 have more than offset the cumulative surpluses of the previous 11 years.

The market imbalance is driven by record demand and stagnant supply growth.

According to the report, global demand rose to a new record high of 1.242 million ounces, up 18% from the record levels seen in 2021. At the same time, the global Silver supply totaled 1.004 billion ounces, roughly unchanged from the previous year. For 2023, supply is expected to grow by 2% to 1.024 billion ounces.

“Silver demand was unprecedented in 2022, and we don’t say that to try and be sensational that is the only way to describe the market,” Philip Newman, Managing Director of Metals Focus, told Kitco News. “The Silver market has entered a new paradigm of deficits that kicked off in 2021.”

Looking ahead, The Silver Institute and Metals Focus expect Silver to post another “sizable deficit” even if it is down from last year’s record highs. Analysts expect solid demand will create a market deficit of 142.1 million ounces in 2023.

“Which would be the 2nd-largest deficit in more than 20 years,” Newman added. “Even if some of the markets are not as strong compared to last year, demand is still expected to be very robust.”

Demand from solar, electric vehicles, and other technological advances will help create the next “Silver Squeeze” this decade. However, the dominant rise of Silver jewelry, once considered out of fashion since the late 2000’s, is now emerging as a formidable challenge to Gold. Its resurgence since early 2023 threatens Gold’s position as the precious metal of choice, with sales of Silver increasing significantly, both in the mid-range and luxury sectors, as well as the second-hand market. As Silver gains momentum and recognition, its sleek and modern allure could potentially lead to decreased demand for Gold.

Dollar Index Short-Term Chart

The Dollar Index run that started in late July topped out at severe resistance at 107 as expected.

It’s very difficult to imagine how the Index will be able to conquer the critical 107 area in an environment where the Fed’s rate hike cycle has ended with the 1st rate cut widely expected as early as March, so a downtrend is in full force and will likely drag the Dollar Index down into the low 90’s at some point in 2024.

For now, though, there is temporary support around 100.50. A reflex bounce out of temporarily oversold conditions to the top of the short-term downtrend line occurred this past week. The declining EMA-50, currently at 103.12, provides additional resistance just above the downtrend line.

RSI(14) bounced off strong support at 30% and may have a tough time getting much above 50% where it is now.

Astute traders will sell into the “relief rally” given the bearish outlook for the greenback in 2024.

Dollar Index Long-Term Chart

The last time the greenback was as hot as we saw for more than a year through September 2022 was during the 2nd half of 2014 into the beginning of 2015. This was a set-up for a big run in Gold and Gold stocks that started in early 2016 and continued for 7 months.

Prior to that, dollar bulls were on a rampage in 2008 (just ahead of a big move in Gold) and from 1999 into January 2001 when the Index briefly touched 120. But early 2001 was also the time to lock in greenback profits and get the heck out of that market as a multi-year slump was about to begin, one that caught so many investors off guard and led to an intense Gold bull cycle.

Fast forward to 2022 and it’s important to note that RSI(14) readings in the summer/early fall last year topped 80%, matching a 25-year high, while the Dollar Index also hit major resistance at 115 at the top of its multi-year uptrend line.

The Dollar Index plunged to a low of 99.22 in mid-July 2023, only to rally back up to 107 in September/October where it encountered very stiff resistance.

A recent move, briefly back above the 200-day SMA currently at 103.33, was reminiscent of late 2016/early 2017 which was quickly followed by a very significant plunge.

%K (Slow Stochastics) has reversed to the downside while RSI(14) is threatening to push below 50% – bad news for bulls.

A -DI/+DI bearish cross has also occurred in the ADX indicator, so a neutral trend is expected to weaken into a bearish trend during Q1.

Watch for a test of the low 90’s in 2024.

Dollar Is Doomed

Fitch Ratings sent shockwaves through the financial world in August when it unexpectedly announced a downgrade of the United States’ credit rating from AAA to AA+. This represents only the 2nd time in U.S. history that a ratings agency has downgraded the country’s debt, the 1st time being when Standard & Poor’s lowered its rating in response to the government’s handling of the 2011 debt ceiling crisis (when Biden was also in the White House).

President Biden’s approval rating has fallen to the lowest level since he took office as Americans are deeply unsatisfied with the state of the economy and how inflation has eroded their financial security, not to mention a host of foreign policy failures. A recent Marquette Law School poll showed how Donald Trump soundly beats Biden among registered voters on policies around inflation, the economy, creating jobs, the border, and foreign relations.

The Biden administration is so frightened (and crooked) that it has weaponized the justice system against its #1 political opponent – how un-American and undemocratic is that? – with the aim to throw Trump in jail or at least derail his campaign. This is a gross example of election interference and 1 of the worst abuses of government power in the history of the United States. It’s also a case of targeting the person, not the crime, which goes against everything America has stood for. Everyday Americans are starting to understand this given Trump’s increasing popularity, despite 4 indictments and some civil cases. Polls and common sense make it clear that he would beat Biden if an election were held today.

Meanwhile, it has become increasingly apparent that Joe Biden, Hunter Biden and other members of the Biden family raked in millions from shakedowns and influence peddling schemes related to Ukraine and other countries, including China, while Biden was Vice-President for 8 years under Obama, concealed through an elaborate network of shell companies (Honest Joe would never take a payment directly of course). Hunter wasn’t always so discrete when it came to some of his payoffs. The total amount of money involved is believed to be at least $20 million to $50 million, perhaps in excess of $100 million, based on House Oversight Committee findings. The “Biden Brand”, being Joe, is what was sold. The corrupt mainstream (state) media, not surprisingly, doesn’t want to report this – The New York Times and The Washington Post won Pulitzer prizes for their coverage of “Russiagate”, the Russia Hoax that was pushed on the American people for more than 2 years, and yet they refuse to investigate highly credible allegations, and very obvious evidence, against Biden and his family. Imagine, for a moment, how the Fake News Media would react if these allegations were against Trump and his family!

Hunter, because he’s a Biden, was shielded from the law for his many indiscretions up until just recently with indictments against him on a litany of charges related to tax evasion and gun violations. The justice system treated him differently than any regular American until now for some reason, perhaps a sign that the politically motivated Justice Department wants a candidate other than Joe Biden to carry the Democrats into next November’s elections.

What a mess – Trump is running for President, facing 700 years in prison potentially on phoney charges, while the current President’s son is now facing the possibility of up to 20 years behind bars for real crimes.

The fresh indictment against Hunter Biden December 7 was followed by a successful vote from House Republican leaders to formally initiate an impeachment inquiry into President Biden over possible ties to his son’s business dealings. House Oversight Committee Chairman James Comer, R-Ky., released subpoenaed bank records showing an entity owned by Hunter Biden had made “direct monthly payments to Joe Biden”.

The Biden family influence peddling scheme will be fully revealed in due course.

Anyway, you don’t have a true or proper democracy when 95% of the media is on 1 side of the political spectrum, favoring the regime and elites in power and collaborating with them. In this case, the mainstream media is playing both defence and offence for the Biden administration – yet the same administration is campaigning that it’s the one “defending democracy” against Trump!

Who’s the real pro-democracy candidate? Don’t forget it was Biden who was slapped by a federal judge for overseeing an “Orwellian ‘Ministry of Truth'”, in the judge’s words, that coerced social media companies into suppressing speech that was at odds with White House policies.

Meanwhile, 2 states have taken the very undemocratic action of taking Trump off the 2024 ballot – Colorado and Maine, with more states to follow unless the Supreme Court puts an end to this insanity which it will likely do next month. Removing Trump from the ballot is based on a perverted interpretation of the U.S. constitution around “insurrection”, without due process of course for Trump. Even the definition of “insurrection” as it pertains to January 6 is a major question mark.

Recently, some in the mainstream media have been ramping up their criticism of Biden – however, that’s only because they’re now fearing the polls, and another Democrat candidate in their view might be needed to prevent “The Evil One” from reclaiming the White House.

The media is exactly what Trump called it years ago, “The Enemy of the People”.

The mainstream media is part of the Establishment Machine assembled by Democrats who will do anything to retain their grip on power – they are the ones who represent the biggest threat to democracy in America. They’re also globalists who will never put America first.

Continuing explosive new evidence regarding potential Biden crimes is being presented by the House Oversight Committee, and also shows how the DOJ and FBI have been protecting Biden who could potentially could get impeached by the House before his term is over. This career politician isn’t what he has pretended to be, and has lied to the American people about his knowledge of his son’s business dealings (greased by the “Big Guy”).

America needs a complete overhaul. The biggest threat to the status quo is Trump – hence, the system’s fear and hatred of him is driving their actions and dividing America like never before.

Ultimately, the greenback could pay a heavy price if a major Constitutional crisis emerges, possible at some point in 2024.

The dollar would also not behave well in an environment of declining interest rates.

Dollar-Centric World Is Over

Iran and Saudi Arabia were among 6 countries invited to join the BRICS block of developing economies January 1 in a move that showed signs of strengthening a China-Russia coalition as tensions with the West spiral higher.

The United Arab Emirates, Argentina, Egypt and Ethiopia also entered BRICS from January 1, joining current members Brazil, Russia, India, China and South Africa to make an 11-nation bloc.

More than 40 countries have expressed interested in joining the BRICS group of nations.

If the world is genuinely starting to witness the demise of the U.S. dollar, countries will have to hold more Gold in their reserves to give their currencies value and stability.

The de-dollarization movement and the general decline of America under an incompetent Biden administration and broken institutions does not bode well for the greenback until at least the November 2024 elections which could very easily produce a Trump victory.

Picking The Right Stocks

It’s easy in a hot market (whether it’s the broader index or individual sectors/stocks) to get greedy and start chasing plays at levels you shouldn’t be chasing them at, and forgetting about the importance of “paying yourself” on regular occasions, and it’s also easy in a difficult or challenging market to succumb to fear. Remember that, and pay close attention to TA and John’s charts – risk-reward ratios are defined through multiple indicators including key resistance and support levels. It’s astonishing how so many investors don’t believe TA applies to penny stocks. In reality, TA applies to anything that has volume. If you ignore TA, or don’t understand it very well, you are greatly reducing your odds of success in this business.

On the fundamental side, a company’s ability to communicate its message clearly is critical! Focus on companies who understand how to relate to investors, who can take something complicated and make it perfectly understandable for the layman! That’s 1 key ingredient we look for in companies we review and that helps explain our success ratio with stock selections.

Below is how we broadly look at Venture companies, and we put a heavy weighting on the communication side and stock behavior. Twenty percent or fewer of Venture companies will score really well on this test:

Management

Expertise and track records, ability to raise capital and execute, trustworthiness, skin in the game, market “friendliness”.

Finances

Working capital, monthly burn rate, transparency, outlook.

Projects

Sector, competitive advantages, scale, grade, conceptual strength, promotability, sizzle, anticipation/speculation potential, geological team, jurisdiction, exploration flow.

Branding/Communications

Effectiveness of “story” and overall brand development, quality of news releases, web site and promotional materials, quality of investor relations/promotion, third party endorsement.

Stock Behavior

Share structure, liquidity, technical strength and posture, short and longer-term price potential, retail backing.

Summary

As you can see above, we use a wide range of metrics to evaluate the prospects for any particular company but we do place a lot of emphasis on management teams that understand how investors think, how markets function, and what it takes to build shareholder value. It’s mystifying that so many CEO’s and management teams of companies listed on a publicly traded and speculative market like the Venture have no clue how to navigate within this sphere! In essence, they are destroyers of wealth, not creators of wealth. Those stocks are like landmines – they can blow up your portfolio in an instant if you’re not careful.

Venture/CSE Trading Tips

It’s imperative to regularly review some basic but essential rules (ignore them at your peril!) about investing in speculative stocks on the Venture and CSE in order to greatly improve your odds of success:

- Always have cash on hand and maintain liquidity to take advantage of sudden pullbacks in the broader market or individual stocks, or great new opportunities that “pop out of nowhere” – that means selling some paper into strength on occasion. You should have a rule that you always maintain a certain level of cash (or instant liquidity) equal to 20% or more of your portfolio value. This will also enforce discipline on you to sell some stocks from time to time, and that’s what most investors struggle with;

- Never buy on margin or invest more than you can afford to lose;

- Let your winners run, but locking in some profits along the way is critical (as the saying goes, bulls and bears make money but pigs get slaughtered);

- Be a contrarian and keep your emotions in check – they are your worst enemy. Many investors who aren’t as successful as they would like to be tend to “follow the herd” – the more prices go up, the more bullish they get; the more prices retreat, the more bearish they get. Understand the trends and play them smartly. Buying low and selling high is the formula for success, but far too many investors do the opposite!;

- Avoid the chat rooms as much as possible – they are full of misinformation and BS, and they mess up your mindset;

- For the Venture, an ideal diversified portfolio would consist of about 10 stocks across some different sectors. Keep it simple – a portfolio that is too big is too hard to manage for most retail investors;

- Always aim to make money serve you – not the other way around;

- Never allow yourself to lose big on one stock – that means don’t be afraid to cut your losses short on a deal if it’s not working out the way it’s supposed to (you will always have some losses, limiting them is key);

- Liquidity and the ability to quickly adapt to changing circumstances are really important;

- When it comes to the Venture, long-term buy and hold strategies very seldom work – stay on top of each stock in your portfolio, technically and fundamentally – you do need to trade!;

- Be aware of “sector rotation” on the Venture – occurs regularly. If you can get in early on a particular sector that’s starting to heat up, profits can be extraordinary;

- The “Efficient-Market Hypothesis” (EMH) is a farce, certainly when it comes to juniors – a Venture stock is either undervalued or overvalued, and investors are making mistakes and overlooking things all the time. You can make a lot of money in this business through patience, discernment and “vision”, and when you remove emotion from your trading;

- Most Venture companies (at least 80%) aren’t worth investing in – focus on the top 5% or 10% of companies who have strong management teams, high quality and exciting projects, and the ability to communicate and promote to the market!;

- In a strong uptrend, always look for Venture support at the EMA(8) and EMA(20) – the same with many individual stocks (those short-term exponential moving averages, and the 50-day SMA, are great buying opportunities on pullbacks as long as they continue to rise). Likewise, during a downtrend, the EMA(8) and EMA(20) will act as resistance on rallies.